Executive Summary (Abstract)

We have found that the current industry and market are among the biggest in the restaurant industry. Amongst the significant and competitive restaurant industry, we can mention the McDonald’s and Cheese Factory are two of the most popular restaurants around us; most people are familiar with these two firms.

This project will dig deeper and compare these two companies’ business strategies, profitability, and risks. We will also investigate their accounting qualities, make financial statements’ forecasts, and firm valuation. In the end, we will conclude which company is a buy.

The Cheesecake Factory and McDonald’s Corporation are two global restaurant chains. Influenced by the Covid-19 pandemic in the restaurant industry, their revenue had been dramatically affected. By comparing the 2020 annual reports of the two companies, we hope to understand the financial status of the two companies and predict the investment value of the two companies.

The Cheesecake Factory Incorporated (CAKE) is one of the leaders in experiential dining. They currently own and operate around 294 restaurants throughout the USA and Canada, including The Cheesecake Factory, North Italia. In addition to that, a collection within their Fox Restaurant Concepts business. Moreover internationally, 27 Cheesecake Factory restaurants operate under licensing agreements. Additionally, their bakery division operates in two facilities which produce quality cheesecakes and other baked products for their restaurants, international licensees, and third-party bakery customers.

McDonald’s, on the other hand, works under an organizational structure designed which supports its efforts toward driving growth (through a Velocity plan they came up with). Additionally, the company’s reporting segments are aligned with strategic priorities so as to reflect the way management reviews and evaluates operating performance. Almost all reportable segments include the United States and International Operated Markets. The Company franchises and operates McDonald’s restaurants, which serve a locally relevant menu of quality food and beverages in 119 countries. Of the 38,695 restaurants at year-end 2019, 93% of them were McDonald’s restaurants.

Module 1

Porter Five Forces Analysis - Cheesecake Factory

- • Industry Competition: The catering industry is a very highly competitive industry. The company’s stores are all over the country, and they need to retain customers by maintaining their advantage, desserts.

- • Buyer Power: Through the location of their restaurants, I think their customer groups are middle-class families. These customer groups will not pay particular attention to food prices but pay more attention to food quality.

- • Supplier power: As a national chain restaurant, their vast supply chain is why they have a price advantage over other competitors.

- • Threat of Substitution: Compared with other chain restaurants, dessert is their specialty and selling point. Their potential competitors may be local pastry shops. However, local pastry shops cannot compete with them in terms of capital.

- • The Threat of Entry: It is difficult for new entrants to pose a threat to them without the support of substantial funds. If they can guarantee the food quality, I don’t think they need to fear any new competitors.

Porter Five Forces Analysis - McDonald’s Corporation

- • Industry Competition: The restaurant industry has a lot many sizes, global chains like KFC. In addition to that, most of the medium and large firms market their products very aggressively. Additionally, McDonald’s customers experience very low switching costs, which essentially means that they can quickly transfer to any other restaurants. Hence, this particular element of the analysis shows that competition is among the most significant external forces on McDonald’s.

- • Buyer Power: Because of the wide variety of customers’ choices, the bargaining power of buyers for McDonald’s is very high.

- • Supplier power: The main reason for the suppliers’ bargaining power for MCD is low because McDonald’s Corporate Social Responsibility strategy including stakeholder management approaches help address these forces from suppliers.

- • Threat of Substitution: The substitution threat for McDonald’s is exceptionally high. Even for McDonald’s products, such as delicacy food producers or local bakeries, there are many other substitutes. Alternatively, consumers can instead cook their food at home as well. It is an elementary shift from McDonald’s to their substitutes (low Switching Cost). Additionally, these substitutes are very competitive in terms of quality and consumer satisfaction.

- • The Threat of Entry: The new entrants threat is moderate because McDonald’s has its brand out there loud and clear for a long history of its business. The smaller restaurant companies are tough to build and get the same brand with some reputation that McDonald’s has. But still, customers can easily switch to other Fast-Food Companies.

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| Accounting Standard | GAAP | GAAP |

| Fiscal Year-end Date | 12/29/2020 | 12/31/2020 |

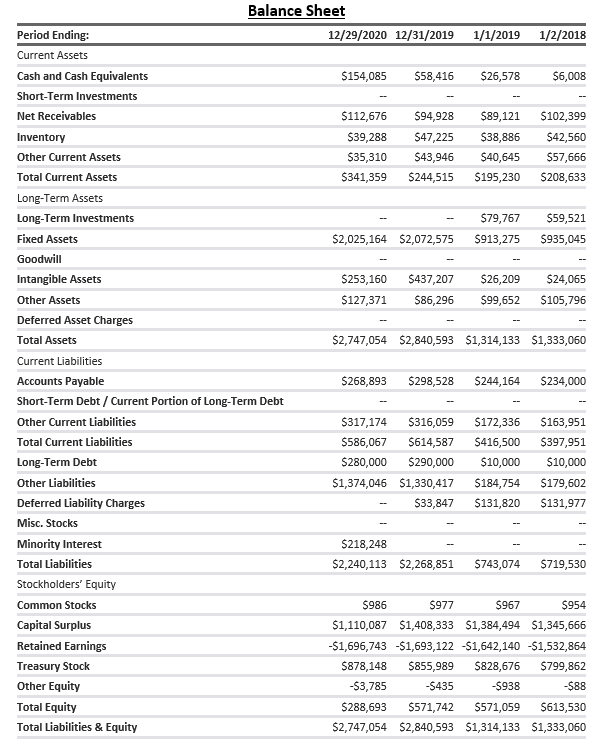

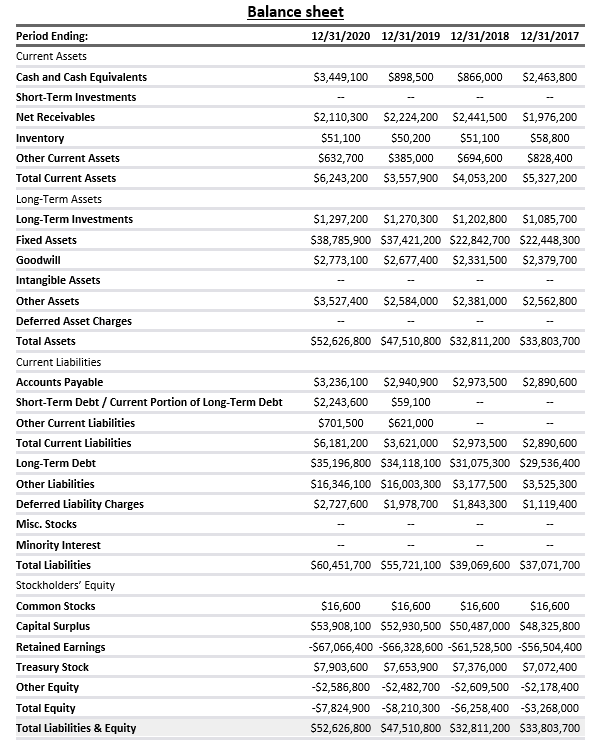

| Short-term Assets | $341,359,000 | $6,243,200,000 |

| Long-term Assets | $2,405,695,000 | $46,383,600,000 |

| Liabilities | $2,240,113,000 | $60,451,700,000 |

| Equity | $288,693,000 | $1,660,000,000 |

| Return on Assets (ROA) | -4.53% | 9.28% |

| Auditing Firm | KPMG | Ernst & Young LLP |

Module 2

Balance Sheet Analysis:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| Largest assets | Property, Plant & Equipment | Property, Plant & Equipment |

| Largest liabilities | Miscellaneous Current Liabilities | Long Term Liability |

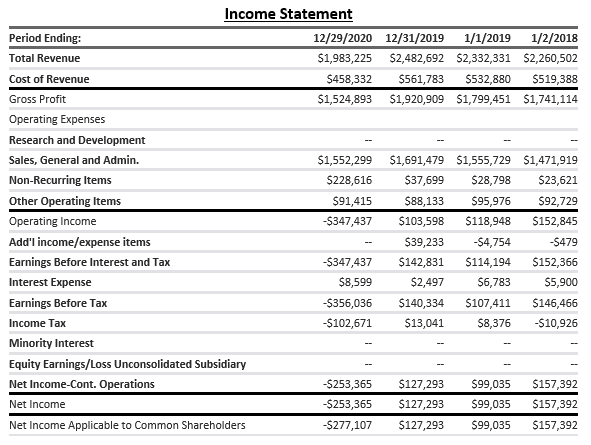

Income Statement Analysis:

- o Major Expenses for Cheesecake Factory: Sales, Admin and General

- o Major Expenses for McDonald’s Corporation: Sales, Admin and General

- o The gross profit of Cheesecake Factory drops:

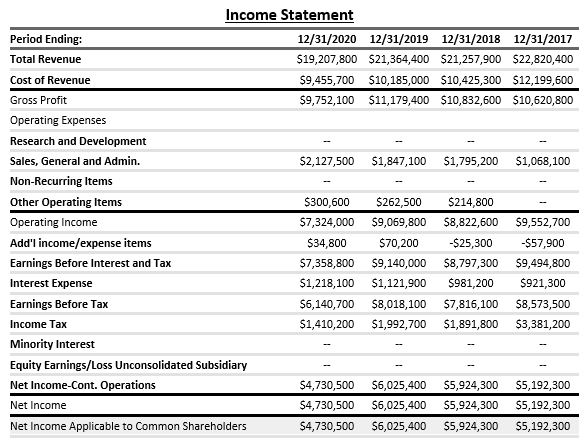

From $1,873 million in 2019 to $1,617 million in 2020 - o The gross profit of McDonald’s Corporation drops

From $11,179.4 billion in 2019 to $9,752 billion in 2020 (12.77% decline)

Statement of Cash Flows Analysis:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

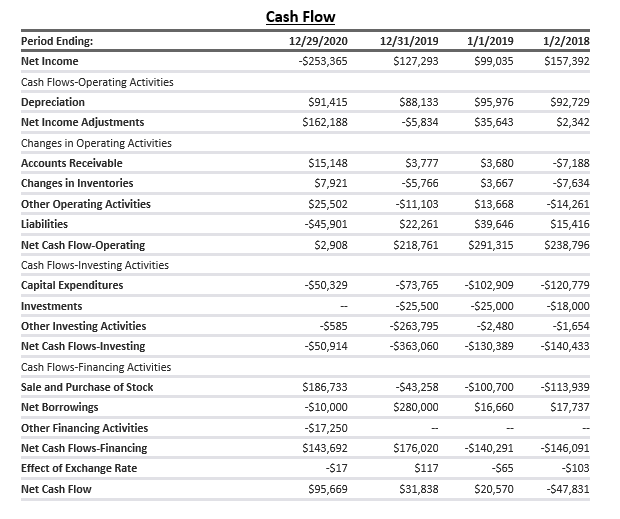

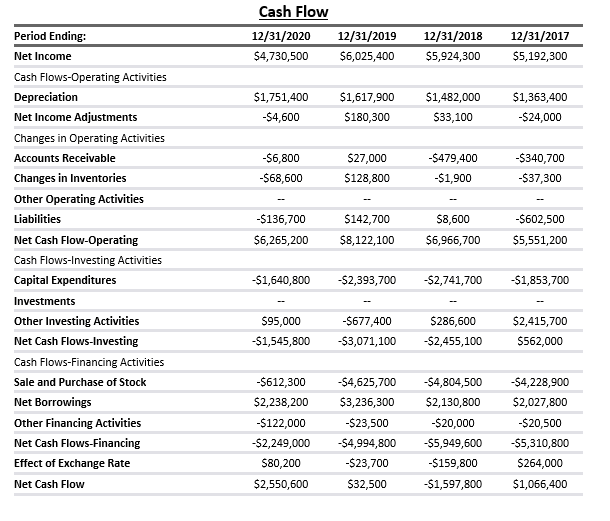

| Net Cash Flow-Operating | $2,908,000 | $6,265,200,000 |

| Net Cash Flows-Investing | -$50,914,000 | -$1,545,800,000 |

| Net Cash Flows-Financing | $143,692,000 | -$2,249,000,000 |

| Net Cash Flow | $95,669,000 | $2,550,600,000 |

Module 3

Return on Equity:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| 2018 | 19% | -100.30% |

| 2019 | 25% | -79.88% |

| 2020 | 0% | 53.99% |

Net Operating Profit Margin:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| 2018 | 0% | 1.36% |

| 2019 | 4% | 0.98% |

| 2020 | 5% | 1.01% |

Current Ratio:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| 2018 | 47% | 1.36% |

| 2019 | 40% | 0.98% |

| 2020 | 58% | 1.01% |

Quick Ratio:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| 2018 | 38% | 1.35% |

| 2019 | 32% | 0.97% |

| 2020 | 52% | 1% |

Cash Ratio:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| 2018 | 47% | 55% |

| 2019 | 40% | 26% |

| 2020 | 58% | 72% |

Liabilities-to-Equity:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| 2018 | 1.30% | -6.24% |

| 2019 | 3.97% | -6.79% |

| 2020 | 7.76% | -7.73% |

Debt/Equity:

| Attribute | Cheesecake Factory | McDonald’s |

|---|---|---|

| 2018 | 0.02% | -6.24% |

| 2019 | 2.59% | -6.79% |

| 2020 | 5.21% | -7.73% |

Module 4

On the 30th of July 2019, the Cheesecake Factory entered into a Third Amended and Restated Loan Agreement which they amended and restated in their prior Second Amended and Restated Loan Agreement which is dated as of the 22nd of December 2015. The Facility, which will be terminated on the 30th of July 2024, provides them which revolves around the loan commitments that total to about $400 million (of which $40 million will be used for issuing letters of credit).

In March 2020, McDonald’s Corporation entered into a 365-Day revolving Credit agreement. The Company borrowed a total of $1 billion (about $3 per person in the US) committed the amount available under the credit agreement. 24th of March 2021 is the maturity date for the revolving credit agreement. The Company borrowed and entered under the Credit Agreement as a precautionary measure to reinforce its cash position while also providing financial flexibility considering the current uncertainty resulting from the COVID-19 pandemic.

MCD also has the entire $3.5 billion commitment from the lenders under the revolving credit agreement which was agreed upon in the “2018 Credit Agreement” and still remains unborrowed. The deal also has representations, covenants, and events of default which are the Credit Agreement does not expire until the 4th of December 2024. Borrowings under the Credit Agreement might be made in U.S. Dollars, or any other agreed-upon currency, at the Company’s option and bear interest at a rate equal to either

Subject to specific conditions which are outlined in the Credit Agreement. According to which, the Company may borrow amounts/prepay/reborrow amounts under the Credit Agreement at any given time during the term of the Credit Agreement. Under the Credit Agreement, McDonald’s is also obligated to pay a facility fee of around 0.375% per annum on undrawn commitments of the lenders. The cost is payable quarterly during the months of February, May, August, and November.

The Credit Agreement additionally contains certain customary representations and warranties and conditional events of default (which includes applicable grace periods). Covenants in the agreement cover insurance, taxes, financial statements, existence, compliance with laws, use of proceeds, and notices of defaults. The Company has also agreed to secure equal and ratable its obligations if the notes issued under the Company’s Debt Securities Indenture, dated as of the 19th of October, 1996, with the U.S. Bank National Association (formerly, First Union National Bank), as a trustee, are secured, or if any other obligation of the Company issued after the date of that Indenture is secured directly or indirectly according to any additional agreement of the company under any provision of that agreement substantially the same as or having an effect substantially the same as the Indenture.

Specific lenders and each of their affiliates have provided and may continue to provide services such as commercial banking, investment management, and other services to the Company, its affiliates, and employees. For that, they receive customary fees and commissions.

Module 5

| 2020 | 2019 | AMT | Increase (Decrease) % | |

|---|---|---|---|---|

| Total Revenue | 1,983 | 2,483 | -500 | -20.14% |

| Expenses: | ||||

| Cost of Sales | 1,922 | 2,181 | -259 | -11.88% |

| SG&A Expenses | 158 | 160 | -2 | -1.25% |

| Total Expenses | 2,080 | 2,341 | -261 | -11.15% |

| Net Income | -253 | 127 | -380 | -299.21% |

| 2020 | 2019 | AMT | Increase (Decrease) % | |

|---|---|---|---|---|

| Total Revenue | 19,207.8 | 21,364.4 | -2,156.6 | -10.09% |

| Expenses: | ||||

| Cost of Sales | 9,455.7 | 10,185 | -729.3 | -7.71% |

| SG&A Expenses | 2,545.2 | 2,229.4 | 316.2 | 14.18% |

| Total Expenses | 11,883.8 | 12,294.6 | -411.3 | -3.34% |

| Net Income | 4,730.5 | 6,025.4 | -1,294.9 | -21.49% |

Module 6

Inventory Analysis:

As a company in the restaurant industry, inventory has an insignificant effect on the two companies. According to their balance sheet, in 2020,

the Cheesecake Factory has $39,288,000 worth of inventory, and McDonald's has $51,000,000 value of inventory.

Tangible Assets:

The fixed assets of both companies are their main assets. According to the 2020 balance sheet, the fixed assets of the Cheesecake Factory equal $2,025,164,000 (about $6 per person in the US),

which has decreased from the previous year. And the fixed assets of McDonald’s increased from $ 2,416,000,000 to $ 2,495,800,000 in 2020.

Restructuring Activities:

The Cheesecake Factory closed three restaurants in 2021, which has a negligible impact on the company. However, because of the impact of the covid-19 pandemic, their operating income has considerably fallen.

McDonald’s is trying to reduce organizational layers from its field staff in the hope of improving communication and providing extra support to its operators, based on the memo McDonald’s published on its website.

The reorganization of MCD began with layoffs and is part of a $500 million administrative and general savings goal announced back in 2015. McDonald’s mentioned that its reorganization would cost around $80 to $90 million this quarter alone, majorly in payment severance and costs associated with the closing of field offices. The company is also eliminating the regional structure it had once in favor of field offices to remove “layers” from its field organization which in turn support franchisees. They said it would increase resources in verticals like technologies and field consulting. They mentioned in its memo that these changes will create a more efficient organization and assist owner-operators succeed. The new field structure should be substituted by the third quarter (from July through September)

In the memo, McDonald’s had also mentioned that the new structure would help the company’s main central office and the field employees often work better with owner-operators. They would also provide more consultations and support for the franchisees and get better at communication between the field staff and the main central office.

McDonald’s also mentioned in the memo that the new structure would perfectly align franchisees with incentives. One of the highest priorities for the company’s field staff would be to improve on the operator cash flow rather than enhancing their sales alone.

McDonald’s hopes that the new alignment with franchisees with incentives will significantly improve the chain’s speed to market. According to them as mentioned in the memo, it would be done by “managing complexity and improving decision-making.”

McDonald’s has been working to improve the speed and efficiency of the deliverability with which decisions on new products or offers goes out to the market to compete with rivals such as Burger King and KFC in a better way, and that has generated strong sales in recent years with the aggressiveness and speed.

McDonald’s said that the new organization would allow them to help with “career progression” internally in the company, allowing and enabling workers and laborers move up the ladder more quickly.

Module 7

| Cheesecake Factory | McDonald’s Corporation | |||

|---|---|---|---|---|

| 2020 | 2019 | 2020 | 2019 | |

| Operating Liabilities | $271 | $286 | $6,181 | $3,621 |

| Main Operating Liability | Accrued Payroll | Accrued Payroll | Accounts Payable | Accounts Payable |

| Total Liabilities | $2,240 | $2,269 | $60,451.7 | $55,721.1 |

| Proportion | 12.1% | 12.6% | 10.22% | 6.49% |

| Cheesecake Factory | McDonald’s Corporation | |||

|---|---|---|---|---|

| 2020 | 2019 | 2020 | 2019 | |

| Short-Term Debt | $0 | $0 | $6,181.2 | $3,621 |

| Long-Term Debt | $280 | $290 | $35,196.8 | $34,118.1 |

| Agency | Cheesecake Factory | McDonald’s Corporation |

|---|---|---|

| Fitch | N/A | BBB |

| Moody’s | N/A | Baa1 |

| S & P | N/A | BBB+ |

Module 8

Contributed Capital:

The total assets financed with the equity are 10.51 (Cheesecake Factory) and 31.702% (McDonald’s Incorporation).

Earned Capital:

Due to the Covid-19 pandemic, the net income of the two companies fell dramatically, and the net income of the Cheesecake Factory was negative.

Therefore, the ROE of the two companies in 2020 has seen a considerable decline compared to the previous year.

Convertible Securities:

On April 20, 2020, in order to increase the liquidity because of the impact of the COVID-19 pandemic on their operations, the Cheesecake Factory had to issue 200,000 shares of series.

A Convertible Preferred Stock, par value is $0.01 per share for an aggregated purchase price of $200 million viz. $1,000 per share.

McDonald’s Corporation did not issue any convertible securities in 2020.

Module 9

Investments in Marketable Securities:

Both companies did not hold any investment. The Cheesecake Factory's annual report revealed that their investment in opening a new restaurant was approximately US$1.7-2 million.

Investments with Significant Influence:

Both companies did not hold any investment.

Investments with Control:

- • Subsidiaries of the Cheesecake Factory:

- - The Cheesecake Factory Restaurants, Inc., a California corporation

- - Fox Restaurant Concepts LLC, an Arizona limited liability company

- - North Restaurants LLC, an Arizona limited liability company

- • Subsidiaries of McDonald’s Corporation:

- Domestic Subsidiaries

- - McDonald's Development Italy LLC [Delaware]

- - McDonald's Deutschland LLC [Delaware]

- - McDonald's International Property Company, Ltd. [Delaware]

- - McDonald's Real Estate Company [Delaware]

- - McDonald's USA, LLC [Delaware]

- - McDonald's Restaurant Operations Inc. [Delaware]

- - MCD Asia Pacific, LLC [Delaware]

- - McDonald's Global Markets LLC [Delaware]

- - Fox Restaurant Concepts LLC, an Arizona limited liability company

- - North Restaurants LLC, an Arizona limited liability company

- Foreign Subsidiaries

- - HanGook McDonald's Co. Ltd. [South Korea]

- - 3072447 Nova Scotia Company [Canada]

- - Limited Liability Company "NRO" [Russia]

- - McDonald's Limited Liability Company [Russia]

- - Moscow-McDonalds [Russia]

- - MCD Europe Limited [United Kingdom]

- - MCD Global Franchising Limited [United Kingdom]

- - MCD APMEA Singapore Investments Pte. Ltd. [Singapore]

- - McDonald's Australia Limited [Australia]

- - McDonald's Franchise GmbH [Austria]

- - McDonald's France S.A.S. [France]

- - McDonald's GmbH [Germany]

- - McDonald's Liegenschaftsverwaltung Gesellschaft m.b.H [Austria]

- - McDonald's Immobilien Gesellschaft mit beschränkter Haftung [Germany]

- - McDonald's Nederland B.V. [Netherlands]

- - McDonald's Real Estate LLP [United Kingdom]

- - McDonald's Polska Sp. z o.o [Poland]

- - McDonald's Restaurants Limited [United Kingdom]

- - McDonald's Suisse Development Sàrl [Switzerland]

- - McDonald's Restaurants of Canada Limited [Canada]

- - McDonald's Suisse Franchise Sàrl [Switzerland]

- - Restaurants McDonald's, SAU. [Spain]

- - McDonald's Suisse Restaurants Sàrl [Switzerland]

The names of a few subsidiaries have been omitted as they do not constitute significantly as they are other domestic and foreign, direct, and indirect subsidiaries of the registrant, which includes 49 wholly owned subsidiaries of McDonald's USA, LLC, many of them operate one or more McDonald's restaurants within the United States and District of Columbia.

Module 10

Capital and Operating Leases:

Most of the restaurants of the Cheesecake Factory are leased. One of the risks they may face is additional costs if they cannot renew their restaurant leases on similar terms and conditions,

or at all, or relocate their restaurants in specific trade areas.

McDonald’s Corporation lease portfolio includes both operating and finance leases; however, as of December 31, 2020, most of the portfolio was classified as operating leases. As the rate implicit in each of the lease is not readily determinable, what the Company uses instead is an incremental borrowing rate to calculate the lease liability which represents an estimated interest rate the Company would incur in order to borrow on a collateralized basis over the lease term within a particular currency environment.

The weighted average discount rate used for leases was 3.8% as of December 31, 2020, and 4% as of December 31, 2019.

As of December 31, 2020, the maturities of lease liabilities for our lease portfolio were as follows:

| Year | 2021 | 2022 | 2023 | 2024 | 2025 | Thereafter |

|---|---|---|---|---|---|---|

| $1230.7 | $1197.7 | $1159.8 | $1124 | $1082.1 | $14295.7 |

- • Total lease payments $20,090.0

- • Less: imputed interest $(6,067.2)

- • Present value of lease liability $14,022.8

Total lease payments include option periods that are reasonably assured of being exercised.

See contractual cash outflows for leases within the Contractual Obligations and Commitments section on page 24. The visible increase in the present value of the lease liability since December 31, 2019, is approximately $0.6 billion.

The lease liability will continue to be impacted by new leases, lease modifications, terminations, reevaluation of lease terms, and foreign currency.

As of December 31, 2020, and December 31, 2019, the Weighted Average Lease Term remaining that is included in the maturities of lease liabilities was 20 years.

Pensions:

The Employees of the Cheesecake Factory are encouraged to invest up to 5% in 401(k) by a top-notch Cheesecake Factory that has a matching program which matches 75% of employees’ contributions.

So, the amount the Cheesecake Factory contributes, it becomes 100% vested after two years, after which the employees can keep even after they have left the Cheesecake Factory.

The McDonald’s Corporation employees are encouraged to invest up to 50% in 401(k). In general, your contributions are limited to $18,500 per year (indexed for inflation in future years). If you are age 50 or older by December 31 in a calendar year, you are eligible for additional “catch up” contributions. The maximum additional catch-up amount is $6,000 for 2018 (indexed for inflation in future years). As a result, the total IRS limit on pretax contributions for participants making catch up contributions is $24,500 in 2018 (indexed for inflation in future years)

Income Tax Disclosures and Strategies:

The Cheesecake Factory’s effective income tax rate was 28.8% and 9.3% in fiscal 2020 and fiscal 2019, respectively Donald’s Corporation effective tax rate was in 2020 compared to the expense of 15.1% in 2019.

McDonald’s annual income taxes for 2020 were $1.41 billion, a 29.23% decline from 2019.

McDonald’s annual income taxes for 2019 were $1.993 billion, a 5.33% increase from 2018.

Final Report

The Cheesecake Factory:

Revenues decreased 20.1% to $1,983.2 million for fiscal 2020 compared to $2,482.7 million for fiscal 2019, primarily due to a decline in comparable restaurant sales, reflecting the impact of the COVID-19 pandemic,

partially offset by additional revenue related to the acquired restaurants and new restaurant openings.

The Cheesecake Factory comparable sales declined by 28.2%, or $601.9 million, from fiscal 2019, driven by a decline in customer traffic of 41.5%, partially offset by average check growth of 13.3%.

Based on balances on December 29, 2020, and December 31, 2019, a hypothetical 10% decline in the market value of the deferred compensation asset and related liability would not have impacted income before income taxes. However, under such a scenario, net income would have declined by $2.2 million and $1.9 million on December 29, 2020, and December 31, 2019, respectively.

McDonald’s Corporation:

McDonald’s annual revenue for 2020 was $19.208B, a 10.09% decline from 2019. McDonald’s annual revenue for 2019 was $21.364 billion, a 0.5% increase from 2018.

The decrease was primarily due to a lower average unit volume driven by comparable restaurant sales. While store weeks increased 2.7% in 2020, similar restaurant sales decreased 14.2%.

The decrease in intermediate unit volumes is primarily due to our dining rooms operating under various limited capacity restrictions due to the pandemic.

McDonald’s Operating margin decreased from 42.45% to 38.13% in 2020. As a percentage of restaurant and other sales, the decrease in operating margin was due to lower sales coupled with higher costs due to the pandemic. In addition, the restaurant margin was pressured by an increase in To-Go sales which typically resulted in a less profitable transaction. See further discussion of specific drivers included below.

McDonald’s annual net income for 2020 was $4.731 billion, a 21.49% decline from 2019. McDonald’s net yearly income for 2019 was $6.025 billion, a 1.71% increase from 2018. primarily due to lower restaurant margin dollars partially offset by lower general and administrative expenses and an income tax benefit.

Conclusion:

The above report shows that the income and revenue of the two companies decreased significantly in 2020, and the cheesecake factory has suffered losses.

For investors, there are significant risks in investing in these two companies now because the pandemic’s impact on these two companies is not over yet.

However, I think McDonald’s has more investment value than the Cheesecake Factory by comparing critical data. For example, McDonald’s has more profitability than the Cheesecake Factory.

At the same time, McDonald’s has a higher cash ratio, Return on equity than the Cheesecake Factory. It indicates that they are at risk of having financial difficulty too.

All in all, I do not think the two companies are good investment targets in the short term. And in the long run, the risk of investing in McDonald’s is lower.

Appendices

Cheesecake Factory Incorporated:

McDonald’s Corporation:

Citations

- 1. https://s22.q4cdn.com/604834465/files/doc_financials/2020/ar/2020-Annual-Report-FINAL.pdf

- 2. https://q10k.com/MCD

- 3. https://content.edgar-online.com/ExternalLink/EDGAR/0001104659-09-056627.html?dest=A09-27588_1EX4DC_HTM&hash=86761be23714a6d9e475f07dcd6e636cd245b2d5bc3b7072c72ebc725e4f8091

- 4. https://www.twomargins.com/c/IBM-2006-10q-hhmsx

- 5. https://content.edgar-online.com/ExternalLink/EDGAR/0001104659-09-056627.html?dest=A09-27588_1EX4DC_HTM&hash=86761be23714a6d9e475f07dcd6e636cd245b2d5bc3b7072c72ebc725e4f8091

- 6. https://www.restaurantbusinessonline.com/financing/mcdonalds-details-its-us-restructuring

- 7. http://apdfs.mergentassets.com/0/1740200.pdf

- 8. https://www.annualreports.com/HostedData/AnnualReports/PDF/NYSE_MCD_2020.pdf

- 9. https://www.benefitspro.org/reports/6708-compare-the-cheesecake-factory-s-employee-health-insurance-and-benefits

- 10. https://dokumen.pub/quantitative-corporate-finance-2nd-ed-9783030435462-9783030435479.html

- 11. https://content.edgar-online.com/ExternalLink/EDGAR/0000063908-21-000013.html?dest=MCD-12312020XEX10V10XK_HTM&hash=febdc2ad7ddd2ca10233cafa532683c7ecffae1c03122862bd9a755cfac71e04